Hot Targets

Which drug targets are surging in patent filings since 2021?

Overview

We split 195,395 patent-target entries into two periods: earlier (1971–2020, across 49 years) and recent (2021–2026, 5 years). By annualizing the filing rates, we can identify targets whose patent activity has exploded — and those that have faded.

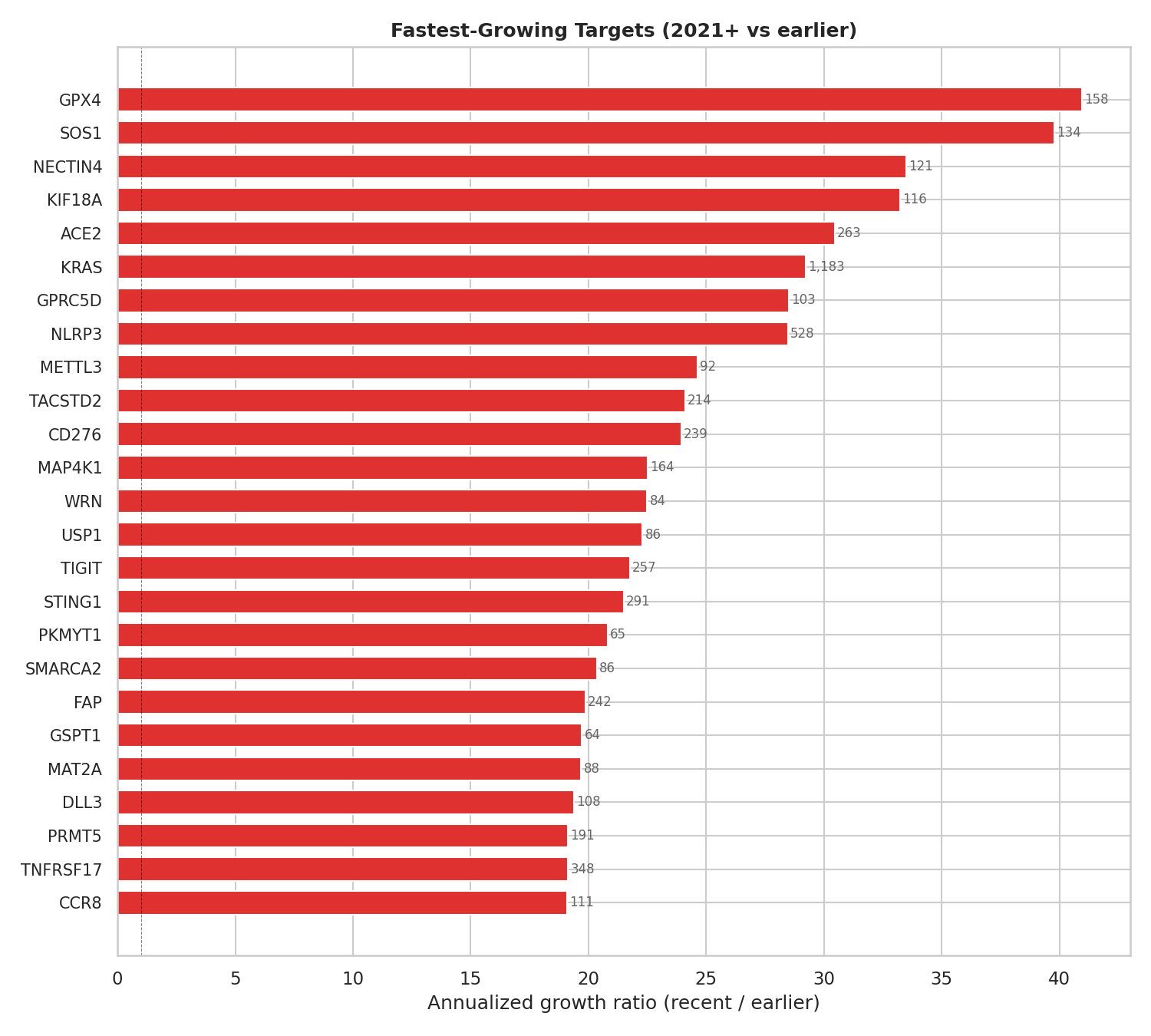

Fastest-growing targets

Growth ratio is annualized: recent filings per year divided by earlier filings per year. A target that went from 1 filing/year to 20/year scores 20x. Only targets with 10+ recent filings are included to filter noise.

| Gene | Role | Pre-2021 | 2021+ | Growth |

|---|---|---|---|---|

| GPX4 | Ferroptosis regulator | 7 | 158 | 41x |

| SOS1 | RAS pathway activator | 3 | 134 | 40x |

| NECTIN4 | ADC target (bladder, breast) | 5 | 121 | 34x |

| KIF18A | Mitotic kinesin (cancer) | 4 | 116 | 33x |

| ACE2 | SARS-CoV-2 receptor | 46 | 263 | 31x |

| KRAS | Oncogenic GTPase | 306 | 1,183 | 29x |

| GPRC5D | Myeloma target (bispecifics) | 5 | 103 | 29x |

| NLRP3 | Inflammasome (auto-immune) | 127 | 528 | 29x |

| TIGIT | Immune checkpoint | 72 | 257 | 22x |

| STING1 | Innate immune activator | 86 | 291 | 22x |

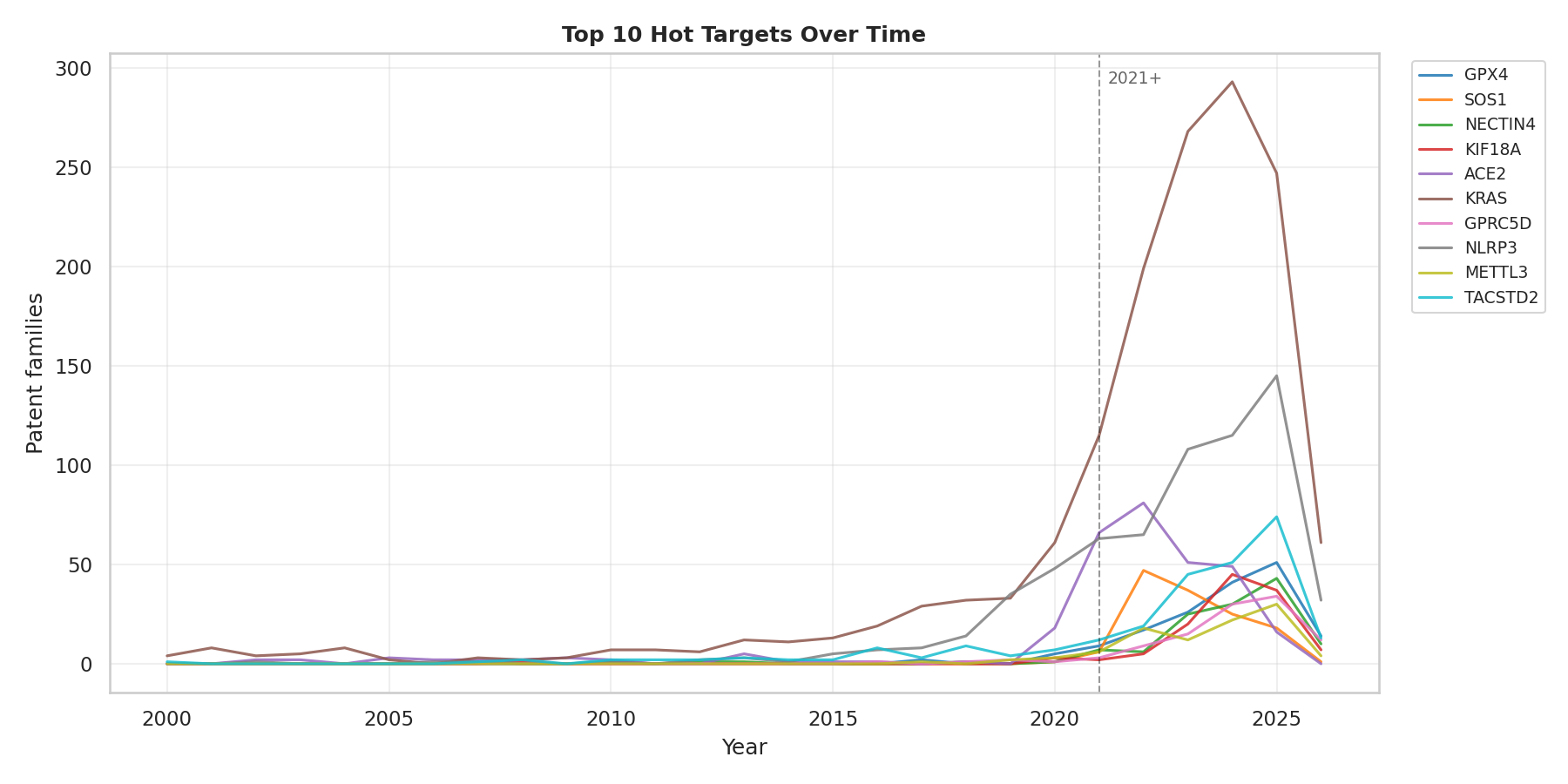

The timeline

Plotting year-by-year filing counts for the top 10 fastest-growing targets shows that most of these surges began around 2018–2020 and accelerated sharply into 2021+. ACE2 has a distinctive COVID-era spike. KRAS shows sustained exponential growth driven by the success of covalent KRAS G12C inhibitors.

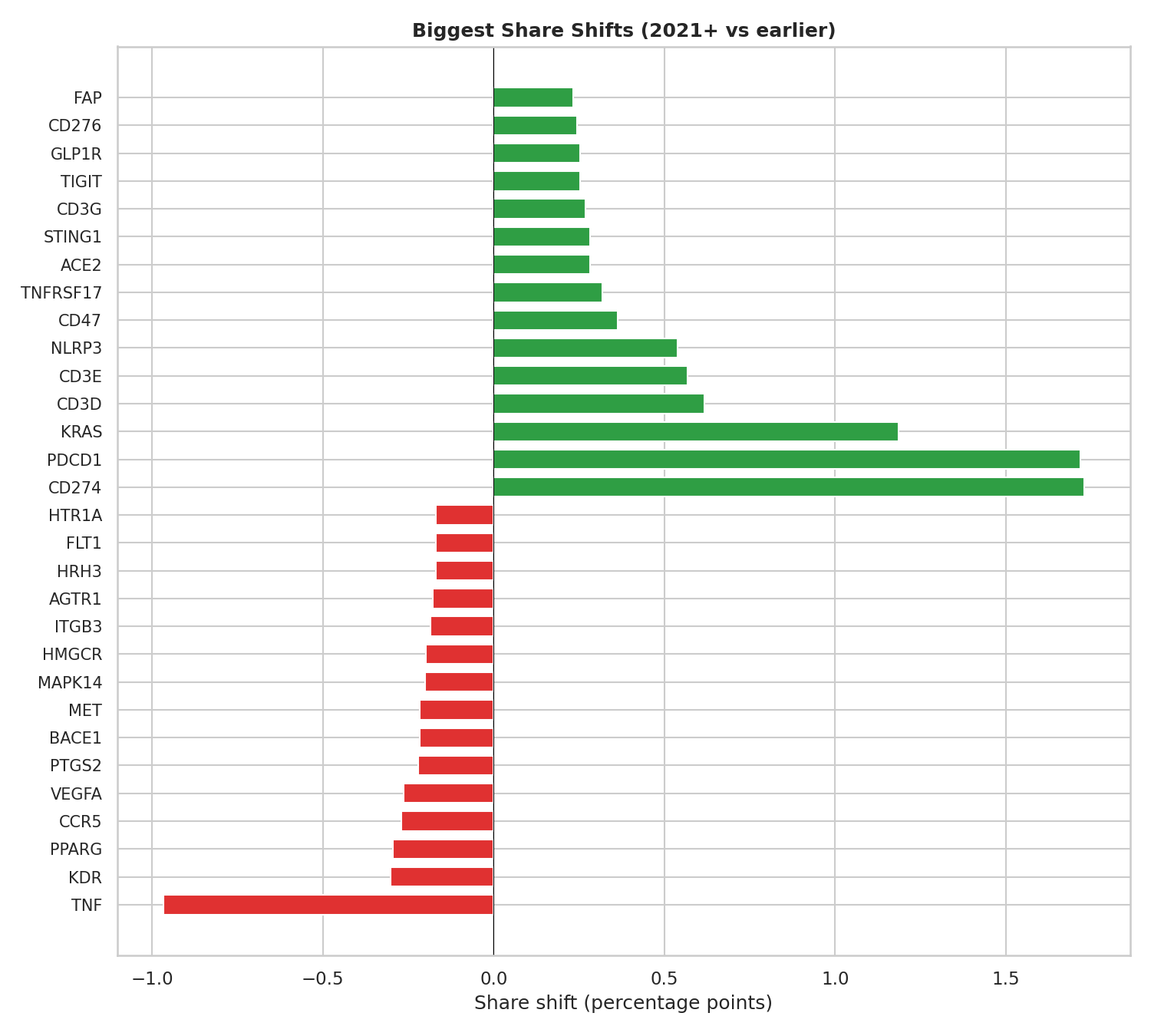

Share shifts

Growth ratio favors small targets that start from near-zero. Share shift measures something different: which targets are capturing more of the overall landscape? A target that goes from 1% to 2% of all filings is gaining real ground, even if its growth ratio is "only" 2x.

The biggest winner is FAP (fibroblast activation protein), riding the radioligand therapy wave. CD276 (B7-H3) and GLP1R (the GLP-1 receptor behind semaglutide) are also major share gainers. On the losing side, TNF, KDR (VEGFR2), and PPARG are giving up landscape share as the field moves on from older target classes.

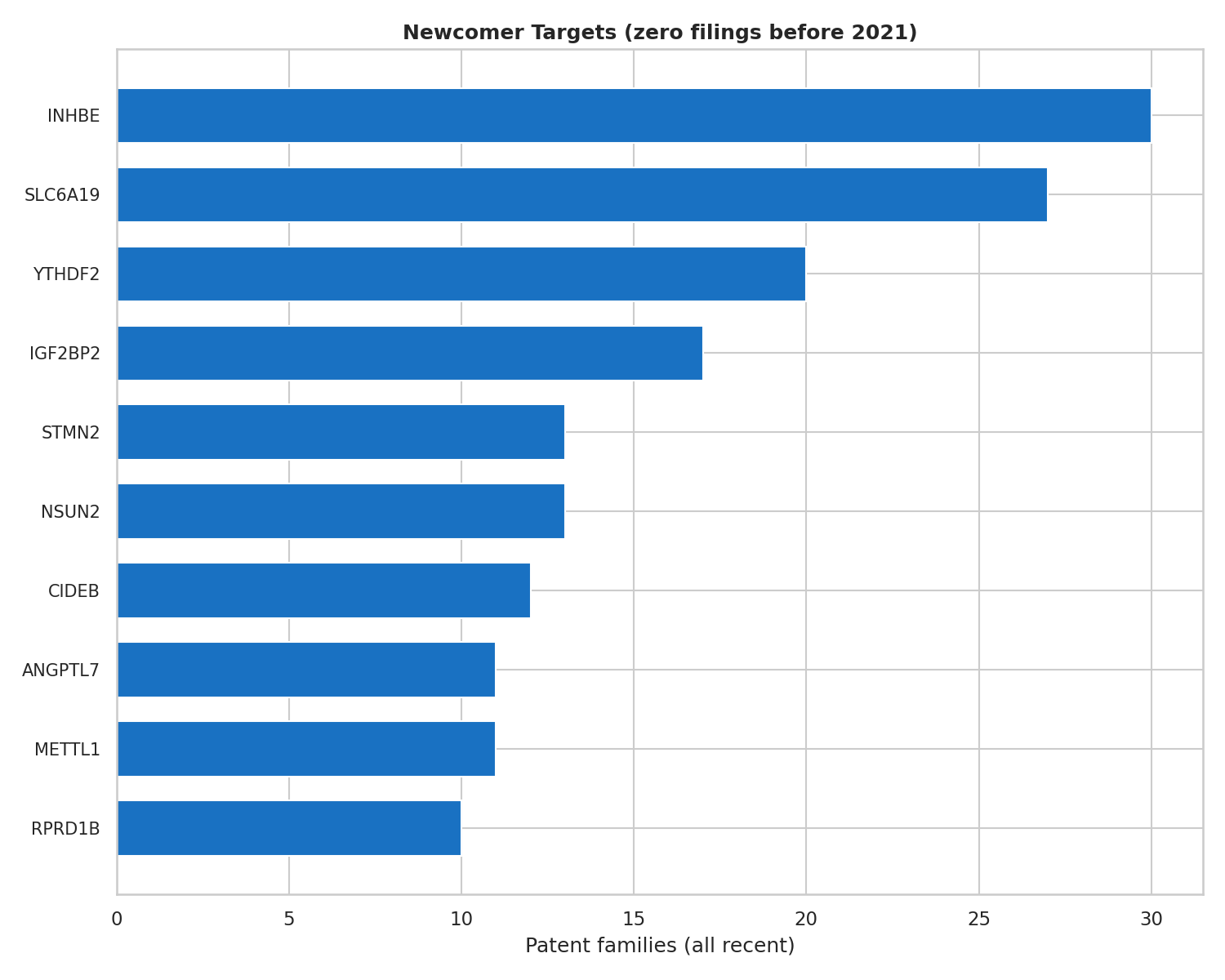

Newcomers

These targets had zero patent filings before 2021 and have emerged entirely in the last 5 years. They represent genuinely new biology entering the drug discovery pipeline.

| Gene | Area | 2021+ filings |

|---|---|---|

| INHBE | Metabolic (activin E, obesity) | 30 |

| SLC6A19 | Amino acid transporter (metabolic) | 27 |

| YTHDF2 | RNA methylation reader (epigenetic) | 20 |

| IGF2BP2 | RNA-binding protein (cancer) | 17 |

| STMN2 | Neurodegeneration biomarker | 13 |

| NSUN2 | RNA methyltransferase (cancer) | 13 |

| CIDEB | Lipid droplet (metabolic/NASH) | 12 |

| ANGPTL7 | Glaucoma / IOP | 11 |

| METTL1 | tRNA methyltransferase (cancer) | 11 |

| RPRD1B | Transcription regulation | 10 |

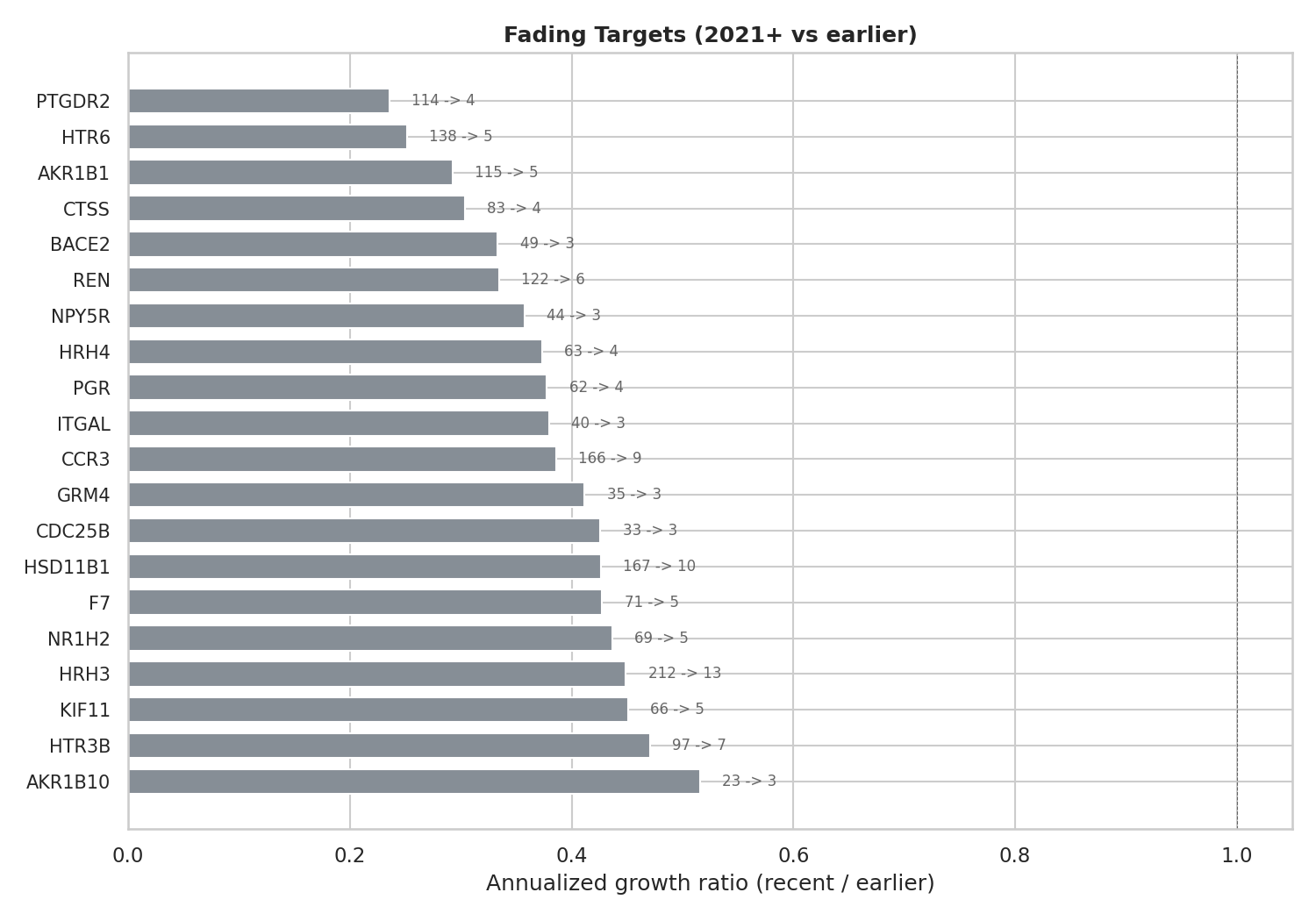

Fading targets

These targets had significant earlier activity but have seen filing rates drop substantially. Many reflect completed drug development cycles — the patents have been filed, the drugs are on market or abandoned, and R&D has moved on.

Takeaways

The RAS renaissance is real. KRAS went from "undruggable" to 1,183 patent families in 5 years, and SOS1 (a RAS pathway enabler) surged 40x alongside it. This is the biggest single-target story in recent biopharma.

Immune oncology is evolving, not declining. PD-1/PD-L1 (PDCD1, CD274) are losing share but still massive in absolute terms. The field is shifting to next-generation checkpoints (TIGIT, CD276, LAG3) and innate immunity (STING1, NLRP3).

Metabolic targets are the new frontier. Among newcomers, INHBE, SLC6A19, and CIDEB reflect the post-GLP-1 gold rush — pharma racing to find the next obesity mechanism beyond semaglutide.

ADCs and degraders are reshaping the landscape. NECTIN4, TACSTD2 (Trop-2), and CRBN (cereblon, for molecular glue degraders) all appear in the top 30. These aren't just new targets — they're new modalities finding new targets.